-

Functional Areas

- Audit and Investigations

-

Capacity development and transition, strengthening systems for health

- A Strategic Approach to Capacity Development

- Capacity Development and Transition - Lessons Learned

- Capacity development and Transition Planning Process

- Capacity Development and Transition

- Capacity Development Objectives and Transition Milestones

- Capacity Development Results - Evidence From Country Experiences

- Functional Capacities

- Interim Principal Recipient of Global Fund Grants

- Legal and Policy Enabling Environment

- Overview

- Resilience and Sustainability

- Transition

-

Financial Management

- CCM Funding

- Grant Closure

- Grant Implementation

- Grant-Making and Signing

- Grant Reporting

- Overview

- Sub-recipient Management

-

Grant closure

- Overview

-

Steps of Grant Closure Process

- 1. Global Fund Notification Letter 'Guidance on Grant Closure'

- 2. Preparation and Submission of Grant Close-Out Plan and Budget

- 3. Global Fund Approval of Grant Close-Out Plan

- 4. Implementation of Close-Out Plan and Completion of Final Global Fund Requirements (Grant Closure Period)

- 5. Operational Closure of Project

- 6. Financial Closure of Project

- 7. Documentation of Grant Closure with Global Fund Grant Closure Letter

- Terminology and Scenarios for Grant Closure Process

- Human resources

- Human rights, key populations and gender

-

Legal Framework

- Agreements with Sub-sub-recipients

- Amending Legal Agreements

- Implementation Letters and Management Letters

- Language of the Grant Agreement and other Legal Instruments

- Legal Framework for Other UNDP Support Roles

- Other Legal and Implementation Considerations

- Overview

- Project Document

- Signing Legal Agreements and Requests for Disbursement

-

The Grant Agreement

- Grant Confirmation: Conditions Precedent (CP)

- Grant Confirmation: Conditions

- Grant Confirmation: Face Sheet

- Grant Confirmation: Limited Liability Clause

- Grant Confirmation: Schedule 1, Integrated Grant Description

- Grant Confirmation: Schedule 1, Performance Framework

- Grant Confirmation: Schedule 1, Summary Budget

- Grant Confirmation: Special Conditions (SCs)

- Grant Confirmation

- UNDP-Global Fund Grant Regulations

- Monitoring and Evaluation

- Principal Recipient Start-Up

-

Procurement and Supply Management

- Development of List of Health Products and Procurement Action Plan

- Distribution and Inventory Management

- Overview

- Price and Quality Reporting (PQR) System

- Procurement of Non-health Products and Services

- Procurement of Pharmaceutical and Other Health Products

- Quality Control

- Rational use of Medicines and Pharmacovigilance Systems

- Strengthening of PSM Services and Risk Mitigation

- UNDP Health PSM Roster

- UNDP Quality Assurance Policy and Plan

-

Reporting

- Communicating Results

- Grant Performance Report

- Overview

- Performance-based Funding and Disbursement Decision

- PR and Coordinating Mechanism (CM) Communication and Governance

- Reporting to the Global Fund

- UNDP Corporate Reporting

-

Risk Management

- Common Risks Identified in Global Fund Programmes

- Global Fund Risk Management

- Introduction to Risk Management

- Overview

- Risk Management in High Risk Environments

- Risk Management in UNDP-managed Global Fund Grants

- Risk management in UNDP

- UNDP Risk Management in the Global Fund Portfolio

- Sub-Recipient Management

Prepare and Finalize a Global Fund Budget during Grant-Making

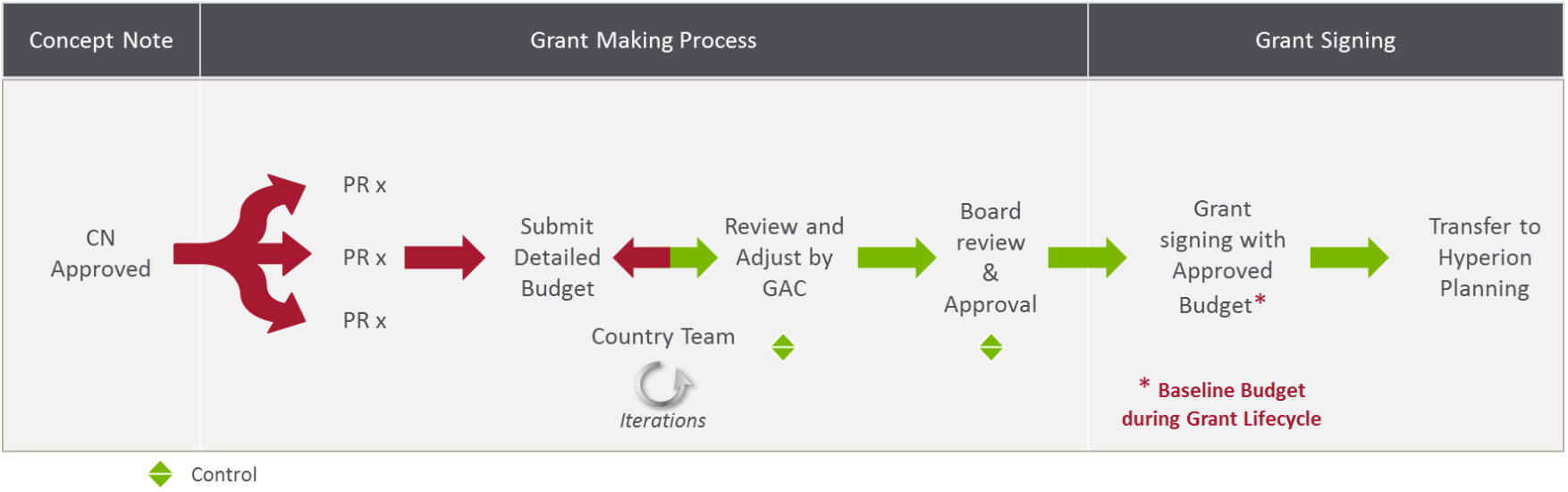

Upon the final approval of a funding request, the nominated Principal Recipient (PR) is required to develop a detailed budget using the full modular approach and costing dimension. Each PR must submit a detailed budget for review and approval, as indicated in the diagram below (Global Fund Guidelines for Grant Budgeting and Annual Financial Reporting - page 24).

As a general principle, in developing a Global Fund work plan and budget, the PR must ensure a strong link between these documents and the performance framework (PF). It is recommended that the PR have a near-finalized PF before developing the budget, to ensure that appropriate levels of funding are allocated to achieve PF objectives/activities and corresponding targets.

In addition, the PR is encouraged to design the work plan and budget with details for each quarter of the grant. It is also recommended that the Programme Manager (whoever is designing the grant) should take the following into account in the template:

- unit cost/number of days/frequency/quantity/implementing partner or entity responsible for implementation (PR/Sub-recipient (SR)/Sub-sub-recipient (SSR));

- cost input linked to each activity line; and

- module and Intervention linked to each activity.

The detailed budget should be based on the cumulative funding approved for the concept note, including any above-allocation funding and any projected in-country cash balance available for the new funding model grant. The budget will provide the following information and justification:

- alignment of the detailed budget to the approved concept note, taking into account any adjustments communicated by the Global Fund following Technical Review Panel (TRP) and Grants Approval Committee (GAC) reviews; and

- quantitative assumptions used for unit costs based on historical data and/or pro forma invoices when necessary.

The detailed budget should be submitted using the Global Fund budget template, which includes the following core information:

- modules – selected from a prescribed list

- interventions – related to the module selected from the prescribed list

- activity – this is not mandatory and is at the discretion of the PR

- implementer – the entity that would implement and manage the associated budget line

- cost input – selected from a prescribed list

- payment currency – this could be in the grant currency, local currency or $ for Euro-denominated grants. The payment currency is the currency that would be used to pay for goods and services. For example, salaries for SR staff funded by the grant should be paid in local currency, health products are paid for in $, etc.

- unit cost at the start of the budget, and annual inflation/increase factor

- quantities required for each period

- period (quarter) – this should be the estimated period of payment and disbursement requirement from the Global Fund. Generally, this excludes procurement lead times for delivery of goods/services/commodities unless there is a specific clause in the grant agreement citing a national legal requirement to access funding prior to the initiation of the procurement process

With respect to SR staff funded by the grant, the following procedures should be followed:

- SRs should contract project staff in local currency without reference to grant currency ($ or Euro).

- The PR is to use the free worksheet in the Global Fund budgeting template to provide the SR salary assumptions in local currency, including projected salary increments based on the inflation rate (not to be completed unless requested by the Global Fund).

- UNDP can request budget adjustments for SR salaries based on the inflation rate in the country. The SR salary adjustments will make use of savings realized due to the depreciation of local currency.

- Country Offices (COs) should agree with Global Fund on reliable sources for inflation data and the procedure for adjusting SR salaries based on the inflation rate.

- Non-material budget adjustments for human resource (HR) costs of less than 5 percent of total budget of recipient HR cost grouping can be made and reported in the Enhanced Financial Report (EFR)/Annual Financial Reporting (AFR) without prior approval of Global Fund. HR cost adjustments above this threshold are considered material and will require prior Global Fund approval.

- The proposed increments for SR salaries denominated in local currency should be included in Progress Update/Disbursement Request (PU/DR) cash forecasts.

The budget template is detailed at:

- Global Fund Guidelines for Grant Budgeting and Annual Financial Reporting – relevant templates at end of document.

- Budget Template Guidelines (Applying for Funding – Grant-making).

- Budget Template (Applying for Funding – Grant-making).

In addition, reference should be made to NFM Budgeting Guidelines.

The total budget must be within the available funding – that is, the allocation amount as adjusted with any above-allocation funds and projected in-country cash balance communicated by the Global Fund. All disbursements between the allocation announcement and the new grant period should be taken into consideration and not included in the budget.

Once the template has been developed, the PR should undertake the following steps to finalize the work plan and budget based on the original document found in the proposal:

- Gather historical data for the grant and country context, in relation to unit costs and organizational arrangements.

- Based on this historical data, clearly define cost assumptions:

- In the absence of historical data efforts must be made to obtain detailed costs for each activity.

- These cost assumptions must be included in the same document for the Local Fund Agent (LFA) and Global Fund to review.

- Analyse the country storage and distribution system to adequately address the weaknesses and costs associated with the storage and distribution of the health products.

- Discuss quantification and procurement and supply management (PSM) assumptions with relevant agencies in the country.

- Consider cost recovery budget lines, as per the UNDP–Global Fund Cost Recovery Agreement.

The work plan and budget will be reviewed by the LFA and the Global Fund, and the PR should prepare for several rounds of negotiations in finalizing this document with the Global Fund. To avoid delays, the PR should take the following steps to ensure a quality work plan and budget:

- confirm the arithmetic accuracy of the budget;

- scan the budget line by line and check details of the unit cost and reasonableness of the assumptions used;

- confirm that budget items are classified in accordance with the Global Fund definitions;

- confirm that the budget is consistent with the proposal and addresses all TRP clarifications;

- confirm that the budget is within the available maximum TRP-approved funding amount;

- identify ineligible costs and confirm inclusion of other mandatory charges;

- confirm that the budget does not contain duplication of funding with other Global Fund grants or other sources of funding;

- confirm the reasonableness of quantities and unit prices;

- seek efficiency gains in accordance with Global Fund Board-mandated requests;

- address the economy, efficiency and effectiveness (value for money) of budget activities;

- confirm that revenue-generating activities are addressed in the budget;

- confirm that the budget is consistent with the proposed programmatic targets in overall terms and on a time basis; and

- provide assurance as to the PR’s ability to absorb and implement the budget within the stipulated time-frame.

Loading resources